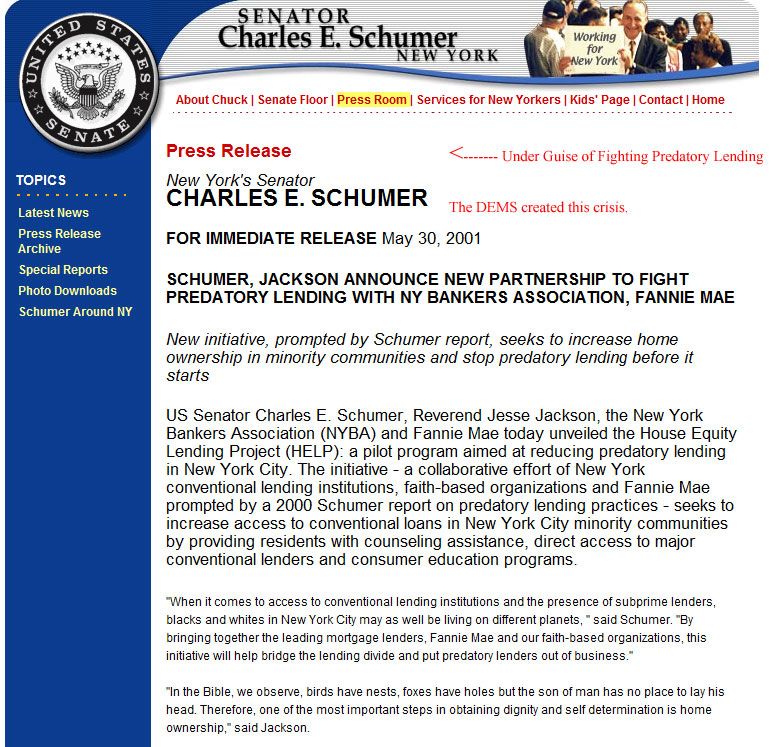

First you must read Robert Bidinotto’s synopsis here:

While Barack Obama was getting campaign contributions from Fannie Mae’s Franklin Raines, John McCain was sounding the alarm about the crisis to come and trying to do something about it. On May 25, 2006, McCain spoke on the floor of the Senate on behalf of his proposed Federal Housing Enterprise Regulatory Reform Act of 2005:

Mr. President, this week Fannie Mae’s regulator reported that the company’s quarterly reports of profit growth over the past few years were “illusions deliberately and systematically created” by the company’s senior management, which resulted in a $10.6 billion accounting scandal.

The Office of Federal Housing Enterprise Oversight’s report goes on to say that Fannie Mae employees deliberately and intentionally manipulated financial reports to hit earnings targets in order to trigger bonuses for senior executives. In the case of Franklin Raines, Fannie Mae’s former chief executive officer, OFHEO’s report shows that over half of Mr. Raines’ compensation for the 6 years through 2003 was directly tied to meeting earnings targets. The report of financial misconduct at Fannie Mae echoes the deeply troubling $5 billion profit restatement at Freddie Mac.

The OFHEO report also states that Fannie Mae used its political power to lobby Congress in an effort to interfere with the regulator’s examination of the company’s accounting problems. This report comes some weeks after Freddie Mac paid a record $3.8 million fine in a settlement with the Federal Election Commission and restated lobbying disclosure reports from 2004 to 2005. These are entities that have demonstrated over and over again that they are deeply in need of reform.

For years I have been concerned about the regulatory structure that governs Fannie Mae and Freddie Mac–known as Government-sponsored entities or GSEs–and the sheer magnitude of these companies and the role they play in the housing market. OFHEO’s report this week does nothing to ease these concerns. In fact, the report does quite the contrary. OFHEO’s report solidifies my view that the GSEs need to be reformed without delay.

I join as a cosponsor of the Federal Housing Enterprise Regulatory Reform Act of 2005, S. 190, to underscore my support for quick passage of GSE regulatory reform legislation. If Congress does not act, American taxpayers will continue to be exposed to the enormous risk that Fannie Mae and Freddie Mac pose to the housing market, the overall financial system, and the economy as a whole.

I urge my colleagues to support swift action on this GSE reform legislation

Robert’s done the best collection of pertinent links, after poking through those please read Lee Cary’s piece on the Obama/Daley housing debacle in Chicago at the American Thinker.

{kind=link}